Are you here looking for the meaning of Adjusted gross income? If yes, then get ready, as this simple guide will provide you with a complete understanding of Adjusted Gross Income and what it means in different situations.

Understanding Adjusted Gross Income

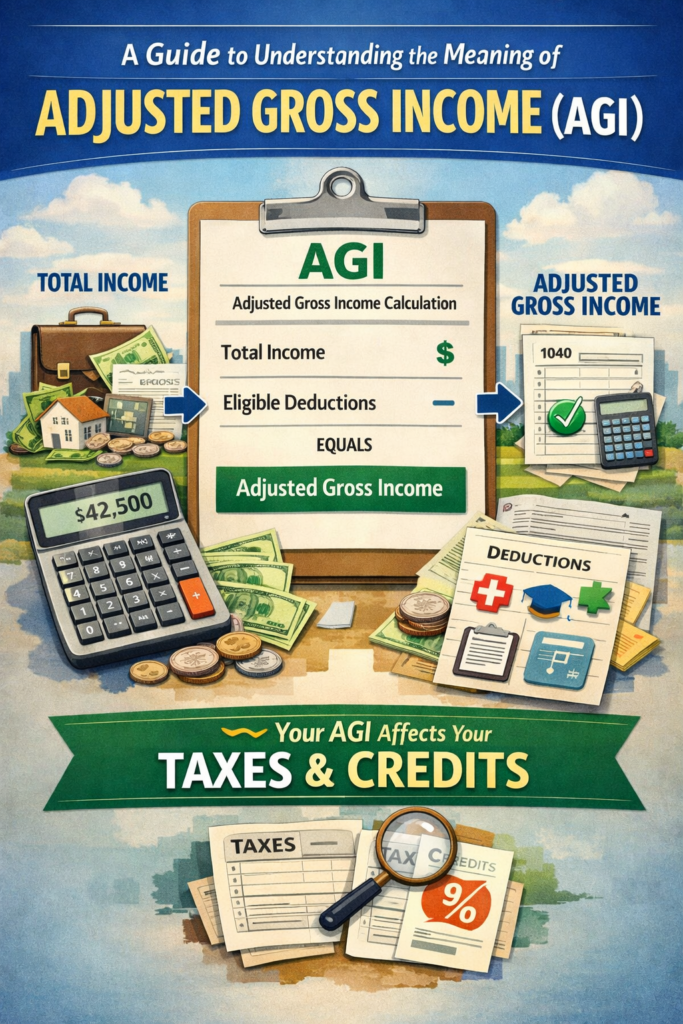

Adjusted Gross Income refers to the total gross income of a person after deducting certain deductions. Along with this, your adjusted gross income is also the starting point from which your taxable income is calculated, as it is also used to determine your eligibility for certain tax credits and deductions that are important for your overall tax bill and tax refund.

Also known as AGI, this term is quite important for tax-related purposes, as it is the point from which your standard or itemized deductions start, which are important for the calculation of your tax liability. With AGI, you can better understand whether you are qualifying for certain deductions or credits. The AGI is also used in other financial situations, such as whether you are eligible to apply for a property loan or you are eligible to rent an apartment.

How do people calculate AGI?

Along with knowing what is Adjusted Gross Income, one of the most important things that you need to know is the process to calculate it. The AGI calculation is rather simple.

The AGI is computed by the total income subject to income tax that you declare, for instance, salary, professional fee, dividend, and bank interest, less specific deductions, or “adjustments” that you are permitted to take. The reporting of your AGI occurs before you take the standard or itemized deductions, which are reported in the later sections of your tax return. This calculation determines the impact of Adjusted Gross Income on W2 tax form.

Adjustments to Income

Adjustments to income are deductions that reduce your income directly to arrive at your AGI. The different kinds of adjustments that you can deduct vary from year to year; however, there are still a few that appear consistently on the filings for taxes every year. These adjustments include:

- The entire amount of the self-employment tax you owe that is not deductible

- self-employed health insurance premiums

- alimony payments made to a former spouse (for agreements before 2019)

- contributions to certain retirement accounts (like a traditional IRA)

- student loan interest paid

- Increases in Deductions and Credits

The Impact of AGI on Deductions and Credits

A lot of the deductions and credits that the taxpayers usually take are limited by AGI. If you choose to itemize deductions, for instance, you need to reduce your medical and dental expenses by 7.5% of your AGI. Thus, it is only the amount that exceeds 7.5% of your AGI that you can claim as a deduction. So, the lower your AGI, the larger the portion of your medical and dental expenses you will be able to deduct.

It is a bit ironic since even some of your adjustments to income are limited by AGI, although those deductions are necessary to calculate your AGI. If you are able to deduct part of your tuition payments, your modified adjusted gross income (MAGI) will be the factor that determines your eligibility.